What's the difference between using a JBLM-focused VA loan specialist and a generic lender for your PCS to Pierce or Thurston County, and how do you choose the right mortgage partner?

A JBLM VA loan specialist understands VA rules, PCS timelines, and local Pierce and Thurston markets, helping you close on time with fewer surprises. A generic lender may offer VA loans but often lacks the PCS, BAH, and local-base expertise you need.

Why Your Lender Choice Matters More During a PCS to JBLM

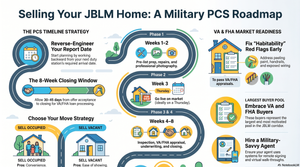

When you're PCSing to Joint Base Lewis-McChord, you don't have the luxury of "figuring it out as you go." You're juggling report dates, temporary lodging, school transfers, and possibly buying and selling at the same time—often from another state or overseas.

The wrong lender can derail a smooth move. Missed closing dates, surprise costs, or a misunderstanding of VA rules can mean extra days in a hotel or TLF, scrambling to extend a lease, storage costs when your HHG beats you to Washington, and extra stress on your family right when you're trying to settle.

The right mortgage partner, on the other hand, works with your orders, BAH, and timeline—not against them. That's where the difference between a true JBLM VA loan specialist and a generic lender becomes critical. Let's break down how to evaluate lenders in Pierce and Thurston County so you can confidently choose a mortgage partner who actually supports your PCS.

1. VA Loan Basics for JBLM Families: What Any Good Lender Must Get Right

Before comparing a JBLM VA loan specialist versus a generic lender, you need a baseline: what every competent VA lender should be able to handle correctly.

Core VA Loan Advantages You Should Expect

Any lender advertising VA loans should clearly explain and correctly apply the core benefits you've earned: $0 down payment with eligible entitlement, no monthly mortgage insurance (PMI), competitive interest rates compared with many conventional loans, flexible credit standards compared to some other loan types, and allowable seller concessions within VA limits that can help reduce your cash to close. If a lender hesitates or gives vague answers when you ask basic questions like "What's my VA entitlement?" or "What are my options with no money down?"—that's an immediate red flag.

Key VA Rules That Must Be Understood

A competent lender should be crystal clear on the VA funding fee—who pays it, when it can be waived (disability rating, Purple Heart while on active duty, etc.), and when it can be financed into the loan. They should understand occupancy requirements: how VA defines "primary residence," and how PCS timelines, TDY, or deployment affect your move-in requirement. They should explain the VA appraisal process including Minimum Property Requirements (MPRs) and how they impact older homes in Tacoma, Lakewood, Olympia, and rural Thurston County. And they should be clear on loan limits versus entitlement—what "no VA loan limit with full entitlement" actually means in practice in higher-priced areas like DuPont, University Place, and parts of Lacey.

If a lender mixes up FHA and VA rules, can't explain VA appraisals, or dismisses your questions with "we'll figure it out later," they might offer VA loans on paper but are not a trustworthy guide.

Basic Questions to Ask Any Lender Up Front

Use these as quick filters before you go deeper: How many VA loans have you closed in the past 12 months? What percentage of your business is VA versus other loan types? How familiar are you with PCS moves to JBLM specifically? Can you walk me through how VA appraisals work in this market? You're not just testing for "right" answers—you're testing for clarity and confidence. If they struggle here, they're going to struggle when your orders or timeline get complicated.

2. What Makes a True JBLM VA Loan Specialist Different From a Generic Lender

Both a big-box bank and a local mortgage broker can say they "do VA loans." But a JBLM-focused VA specialist brings specific experience that matters when you're moving into or out of Thurston and Pierce County on military orders.

Deep Familiarity With PCS Realities

A true JBLM VA loan specialist understands how to use your BAH, LES, and even future duty station pay information where guidelines allow. Rather than offering a generic "30 days to close," they ask: "When do you sign out from your current duty station? When do you report to JBLM?" They have systems for e-signatures, remote underwriting, and clear communication even if you're OCONUS.

For example: if your report date to JBLM is October 1st, a JBLM VA specialist will help you target a closing date that gives you time to get keys, schedule HHG delivery, and avoid doubling up on rent and mortgage if possible. A generic lender might simply offer the next available closing date that works for their pipeline—not your orders.

Local Market Knowledge Around JBLM

JBLM straddles Pierce and Thurston Counties, and each sub-market has its own quirks. In Pierce County—Tacoma, Lakewood, Puyallup, DuPont, Spanaway—you'll find older housing stock in some areas with appraisal and MPR implications, and strong competition in certain neighborhoods that requires fast, clean approvals. In Thurston County—Lacey, Olympia, Yelm, Tumwater—military families often seek newer homes with slightly more space, and some rural properties have wells or septic systems that can trigger additional VA scrutiny.

A JBLM VA loan specialist anticipates these issues before you write an offer. They'll flag potential VA MPR red flags on an older Tacoma bungalow—peeling paint, missing handrails, roof condition—and explain why a rural Yelm property might require extra time or documentation due to well and septic inspections.

Coordination With Military-Savvy Real Estate Pros

Specialists who regularly serve JBLM families maintain strong relationships with local REALTORS® experienced with VA, understand typical PCS closing timelines in this area, and know how to explain VA-specific items—like the VA amendatory clause, non-allowables, and appraisal conditions—to both your agent and the listing agent. By contrast, a generic lender may treat your file like any other purchase, without appreciating how a delayed appraisal or extended underwriting can ripple into your PCS schedule, TLF availability, and family logistics.

3. How Your PCS Timeline Changes the "Right Lender" Decision

Not every PCS to JBLM looks the same. Your personal situation—buying while deployed, selling and buying simultaneously, or investing while you're still stationed here—changes which lender will truly fit you.

Scenario 1: You're Buying From Out of State or OCONUS

If you're house-hunting from another duty station or overseas, you need strong digital communication with regular updates and quick answers via email or secure messaging, time zone awareness from a team that respects your schedule, and comfort with remote underwriting from processors used to reviewing LES, BAH, and military income documentation without asking for unnecessary paperwork.

A JBLM VA loan specialist has likely managed many sight-unseen or video-tour purchases for JBLM-bound families. They'll be proactive about locking your rate at the right time, coordinating with your agent, and making sure your pre-approval is strong enough to win in competitive neighborhoods like DuPont, Lacey, or University Place.

Scenario 2: You're Selling a Home Near JBLM and Buying Another

If you already own a home in Pierce or Thurston County and are trading up, downsizing, or relocating within the area, your lender needs to handle equity and timing coordination—bridge options, using proceeds from your current sale, or structuring closing dates so you don't end up without a home for a week. They should also understand how your remaining entitlement works if you still have an existing VA loan, and how to help your agent present a strong file even if your purchase is contingent on your sale.

Generic lenders sometimes stumble here, especially around the nuances of partial entitlement and calculating your maximum VA loan amount while another VA loan is still active or recently paid off. A JBLM specialist will map out the numbers and timelines before you list your current home.

Scenario 3: You're Investing While Stationed at JBLM

Many service members and veterans use their VA benefits strategically to build long-term wealth—buying a home while stationed here, then keeping it as a rental after PCSing out. In that case, the right lender should explain how VA occupancy rules work if you plan to rent the property after you move, help you think through cash flow versus BAH while you're stationed here, and provide clarity on future financing options once your VA entitlement is partly tied up in a local rental.

A JBLM VA loan specialist can also flag local considerations like rentability in different school districts, commuting patterns, and how certain HOA rules or condo projects may or may not be VA-approved. Consulting a tax professional about rental income implications is always advisable before making that decision.

4. JBLM VA Loan Specialist vs Generic Lender: Side-by-Side Comparison

It helps to see the differences in clear, practical terms.

Experience and Focus

A JBLM VA loan specialist has a high percentage of business in VA and military moves, is familiar with BAH tables, LES formats, and common PCS scenarios, and regularly works with buyers in Lacey, Yelm, DuPont, Lakewood, Tacoma, and Olympia. A generic lender treats VA loans as just one product among many, has limited experience with PCS complexity and military pay structures, and may not know local neighborhoods or typical appraisal issues.

Communication and Timing

A specialist starts by asking about your orders, report date, and family needs; builds a backwards timeline with underwriting, appraisal, and closing aligned to your PCS; and prepares your file early to avoid last-minute surprises. A generic lender focuses first on generic pre-approval numbers, uses standard timelines that may not account for your move date or TLF limitations, and is more likely to request additional documents late in the process.

VA-Specific Strategy

A specialist strategizes to minimize out-of-pocket costs using VA rules appropriately, understands funding fee exemptions and ensures you're not overpaying, and flags homes that may struggle with VA appraisal or MPRs before you're under contract. A generic lender treats VA rules as a checklist rather than a planning tool, might overlook potential funding fee exemptions or miscalculate your entitlement, and may let you write offers on properties that later hit VA appraisal obstacles.

Local Coordination

A specialist has existing relationships with local REALTORS®, title and escrow, and inspectors who understand VA; can often get informal heads-up on appraisal timing and local conditions; and understands commute patterns to JBLM gates. A generic lender often has centralized processing with no local presence, is less able to coordinate quickly with on-the-ground partners, and provides numbers but little local guidance or nuance.

5. How to Interview and Choose the Right Mortgage Partner for Your JBLM Move

You don't need to become a mortgage expert to protect yourself. You just need to ask the right questions and pay attention to how lenders respond.

Step 1: Ask About Their Experience With JBLM and VA Loans

Ask how many VA loans they've closed in this area in the past year, what proportion of their clients are active-duty or veterans, and whether they can describe a challenging PCS loan they handled and how they kept it on track. Look for specific numbers rather than vague answers, real examples showing they've navigated PCS delays, changing orders, or remote buyers, and familiarity with JBLM specifically—not just "Washington State" in general.

Step 2: Clarify Timelines and Communication

Ask what their typical closing timeframe is for a VA purchase here, how often you'll hear from them during the process and in what format, and who your main point of contact will be—a direct line or a call queue. You want a realistic, conservative closing timeframe that still meets your PCS needs, a clear communication plan with weekly updates and milestone check-ins, and a named loan officer or team rather than just "our department."

Step 3: Test Their Local Knowledge Without Leading Them

Ask whether there are common VA appraisal issues in homes near JBLM to watch for, whether they see important differences between buying in Pierce versus Thurston County with a VA loan, and how wells, septic systems, or older homes impact VA financing here. A JBLM specialist will have detailed, practical answers. A generic lender might respond with broad comments or say "it just depends" without context.

Step 4: Compare More Than Just the Interest Rate

Of course, compare interest rates, lender fees, and estimated closing costs. But also weigh reliability to close on time (crucial for PCS), quality of explanations and advice, and your overall comfort level and trust. A slightly lower rate doesn't help if a lender's delays force you into extra hotel nights, storage fees, or a contract extension. Under Fair Housing, RESPA, and related regulations, always review official Loan Estimates from multiple lenders before deciding so you can compare on disclosed terms and services.

FAQ: JBLM VA Loan Specialist vs Generic Lender

Is it better to choose a local JBLM VA loan specialist than a big national lender?

Not all national lenders are bad, and not all local lenders are outstanding. However, a lender—local or national—who specializes in VA loans and routinely serves JBLM families usually offers smoother PCS-aligned timelines, better understanding of VA guidelines, and more relevant advice about Pierce and Thurston County markets than a generic lender who rarely works with military borrowers.

Can I use my VA loan to buy a home near JBLM if I might rent it out after my next PCS?

Yes, many JBLM service members buy with a VA loan, live in the property as their primary residence while stationed here, and later convert it to a rental after PCSing. Your lender should clearly explain occupancy requirements, timing, and how turning the home into a rental affects your future VA entitlement and borrowing power. Be honest about your plans, follow VA rules, and consult a tax professional about rental income implications.

What if I'm already under contract with a generic lender and things aren't going well?

You can switch lenders in many cases, but you need to consider where you are in the process, your contract deadlines, and whether a new lender can realistically close on time. Before making any changes, talk openly with your current lender about your concerns, then consult a JBLM-experienced VA specialist to compare timelines, costs, and feasibility. Always coordinate with your real estate agent and review your purchase contract to avoid breaching any terms.

Bringing It All Together for Your JBLM PCS

Choosing between a JBLM VA loan specialist and a generic lender is really about choosing the kind of PCS experience you want for your family. You've already got enough on your plate—orders, kids, pets, cars, HHG, maybe even a spouse deploying or changing jobs at the same time.

A true JBLM VA loan specialist brings three things that matter most: deep understanding of VA rules and how to use them to your advantage; respect for your PCS timeline and the realities of military life; and familiarity with Pierce and Thurston County markets, from Tacoma and Lakewood to Lacey, Yelm, and Olympia.

When you interview lenders, listen for evidence of that experience—not just good sales talk. Ask about their work with JBLM families, how they handle VA appraisals in this area, and how they'll keep your PCS closing on track. If you take the time now to choose the right mortgage partner, you'll be in a much better position to arrive at JBLM, pick up your keys, and start making your new home in Pierce or Thurston County feel like home—without wondering whether your lender is the weakest link in your move.

Work With PCS Home Group's JBLM-Connected Team

At PCS Home Group, we work alongside VA-experienced local lenders every day—and we know which ones consistently close on PCS timelines and communicate like partners, not strangers. Our team brings:

Ashleigh Camberg's strategic leadership: Deep VA loan knowledge, PCS-aware systems, and relationships with lenders who understand what JBLM families actually need

James Camberg's market analysis: Hyperlocal comp data across Pierce and Thurston County so your purchase decision is grounded in real numbers—not guesswork

Kelly Barron's neighborhood intelligence: Micro-market expertise from DuPont to Lacey to Yelm so you can weigh location trade-offs with confidence

When you're ready to build your JBLM mortgage and real estate team, we'll help you ask the right questions and connect with the right people—so your PCS goes the way it should.

Ready to talk through your JBLM VA loan and home search options?

Contact Ashleigh Camberg:

Phone: (360) 513-9034

Email: acamberg@pcshomegroup.com

Visit: pcshomegroup.com

Meet the team: pcshomegroup.com/team-page