What's the smartest way for JBLM military families to choose and vet the best VA loan lender and real estate agent in Pierce and Thurston County?

The best team for JBLM families combines deep VA loan expertise, PCS-aware timelines, local market knowledge, and transparent communication. Vet them by their VA track record, reviews, the questions they ask you, and how they handle inspection, appraisal, and short-notice moves.

Why Your Local VA Loan and Real Estate Team Matters So Much at JBLM

If you're PCSing to or from Joint Base Lewis-McChord, you don't have time or money to waste on the wrong lender or agent. You're juggling orders, kids, pets, HHG shipments, leave windows, and maybe a spouse who's still downrange or at another duty station. One missed deadline or weak lender letter can mean losing the home you need—right when you need it.

At the same time, the Tacoma–Lakewood–Lacey–DuPont–Yelm–Puyallup corridor is one of the most competitive markets in the Pacific Northwest. Inventory moves fast. VA loans are powerful, but if your lender or agent doesn't know how to write and present a strong VA-backed offer, you can get pushed aside for conventional buyers—even when your offer is stronger on paper.

That's why you can't just grab whoever a relocation site suggests and hope it works out. You need a local, VA-savvy team that understands BAH, COLA, and your PCS timeline; knows which neighborhoods work with your commute, schools, and budget; can explain VA appraisal, minimum property requirements, and zero-down offers clearly; and has a proven system for remote buyers, sight-unseen offers, and tight reporting dates. The good news: when you know what to look for and how to vet people, you can quickly separate true pros from agents or lenders who do one or two VA deals a year.

1. What Makes a Great VA Loan Lender for JBLM Families?

Not all mortgage lenders are created equal—especially when it comes to VA loans in a military-heavy market like JBLM. A great lender for you is not just the one with the lowest advertised rate; it's the one that can actually close your VA loan on time, with clear communication, and no last-minute drama.

Key Signs Your Lender Truly Understands VA Loans

When you talk to a potential lender, you're trying to confirm they live and breathe VA lending—not that they "can do them if needed." Ask pointed questions: "What percentage of your monthly business is VA loans?" "How many VA transactions did you close in the last 12 months?" "How often do you work with JBLM buyers specifically?"

Look for answers that show VA is a core focus—30–50% or more of their pipeline is VA, dozens of VA deals each year, and specific JBLM examples with familiarity with DuPont, Lacey, South Hill, Spanaway, Yelm, and Steilacoom. You also want them to explain VA-specific topics in plain language: VA funding fee and who is exempt, how your disability rating impacts your costs, minimum property standards and how they affect older homes and rural properties, and VA appraisal process and realistic timelines in Pierce and Thurston County. If they stumble on these or give vague answers, keep looking.

Local Versus National VA Lenders

Many big-name online or national "VA specialists" run high-volume call centers. They might offer attractive marketing, but for JBLM buyers, the trade-offs matter. Local and regional VA lenders typically offer direct contact with an actual loan officer and in-house underwriter, understanding of local appraisal turn times and common VA issues (well and septic, outbuildings, older homes), relationships with local agents and title and escrow, and willingness to call a listing agent directly to vouch for you and your pre-approval. National lenders may offer aggressive promotions, but the downside is often rigidity and slower response when a local listing agent needs answers. In a bidding war, a strong local VA lender who can pick up the phone on a Sunday and explain your file can make the difference between accepted and rejected.

How to Stress-Test a Lender Before You Commit

Don't wait until you're under contract to find out your lender can't keep up. When you first talk, time their response—how fast do they reply to your first inquiry, and do they answer after hours or on weekends when most of your house hunting will actually happen? Evaluate their questions: pros will ask about your PCS report date and likely arrival, whether you'll be on leave or TDY during the process, your current lease end date or home sale timeline, and your long-term plans (renting the home out later, retiring in the area).

Ask for a detailed pre-approval, not just a pre-qualification—have they pulled credit, reviewed your LES, orders if available, and income documents? Will they issue multiple pre-approval letters quickly as you adjust offers? And confirm closing speed and track record: "What's your average VA closing timeline in Pierce and Thurston right now?" and "When was the last time you missed a closing date on a VA loan, and why?" A lender experienced with JBLM families will have concrete answers—and shouldn't be offended by these questions.

2. How to Choose a VA-Savvy Real Estate Agent Around JBLM

Your real estate agent is the other half of your local team. For VA buyers and sellers near JBLM, you need more than someone who simply has a license. You want someone deeply familiar with VA financing, experienced with PCS timelines and remote decision-making, and actively working in the JBLM-adjacent markets you care about.

Questions That Reveal True VA and PCS Expertise

When you interview agents, treat it like hiring for a critical role—because that's exactly what it is. Ask what percentage of their clients are active-duty, Guard/Reserve, or veterans; how many VA-financed transactions they closed last year; how they handle a VA appraisal issue; and how they help buyers who are house-hunting from out of state or overseas.

Listen for specific examples: stories about negotiating repairs after a VA appraiser flagged safety items, experience with tight windows between report date and closing, and systems they use for virtual showings, video walkthroughs, and e-signing. If their answers sound generic—"I've worked with the military before" without details—keep interviewing.

Local JBLM Market Knowledge You Should Expect

A strong JBLM agent doesn't just know the MLS—they know what daily life looks like for you. They should be able to talk through commute patterns including gate hours and traffic for North Fort, Main Gate, East Gate, DuPont, and I-5 choke points; common duty locations and what that means for where you live; and neighborhood pros and cons including DuPont and Steilacoom for shorter commutes and walkability, Lacey, Olympia, and Tumwater for school choices and amenities, and Yelm, Roy, and Graham for more land and lower prices with longer drives.

Ask them: "What would you recommend for a family of four with one kid in middle school, one in elementary, working on Lewis Main, and wanting a 30–40 minute max commute?" Their answer will tell you whether they're guessing or actually mapping your lifestyle to specific neighborhoods.

Evaluating How Your Agent Negotiates With a VA Loan

Some listing agents still hold outdated beliefs that VA offers are harder or weaker. A good buyer's agent knows how to counter that. Ask how they present VA offers to listing agents in multiple-offer situations and whether they've successfully gotten VA buyers accepted over conventional buyers and how. They should discuss strongly written pre-approval letters and lender calls to the listing agent, structuring earnest money, inspection timelines, and closing dates to be attractive, and clarifying that VA loans are not harder—just slightly different on appraisal and condition.

If you're selling and the buyer has VA financing, your listing agent should explain what repairs are truly required versus negotiable, how to prepare the home to avoid VA appraisal delays, and how to manage expectations on both sides while following Fair Housing and anti-discrimination laws.

3. Red Flags When Choosing JBLM VA Lenders and Agents

Knowing what to avoid is just as important as knowing what to look for.

Red Flags With VA Loan Lenders

Watch out for lenders who minimize or rush your questions—"Don't worry, we'll handle it" without explanation is a problem. Vague comments about "the appraisal people" or "some extra VA steps" show they don't have a clear process. Unrealistically low rates without fees are also a warning sign: always ask for a written fee breakdown, an estimate of total cash to close, and clarity on whether you're seeing points or lender credits.

If they never ask about your orders, travel dates, or whether one spouse will be unavailable for signatures, they may not be used to military timelines. And slow response during pre-approval often turns into major panic during underwriting—take note of how quickly they communicate from the very first contact.

Red Flags With Real Estate Agents

You may be talking to the wrong agent if they talk down VA loans—comments like "VA is a pain, but we can try" or "sellers don't like VA" often come from lack of understanding, not facts. VA is a strong benefit and should be treated that way. Watch for agents who don't ask detailed questions about your PCS; they should want to know when you report, whether you're buying sight-unseen, if you might rent the home out later, and whether you've used your VA entitlement before.

Be cautious of agents who seem pushy about new construction or a single builder—if all their suggestions point one direction, ask why. And watch for promises they can't control: guarantees about future resale value, winning the first offer, or VA approving any home. A good agent can give educated opinions but should acknowledge market risks and VA guidelines honestly.

Compliance and Fairness Considerations

Any professional you work with should respect Fair Housing laws—they shouldn't steer you toward or away from neighborhoods based on protected classes. They can discuss commute, features, price, and data, but not "types of people" in an area. Under RESPA, they may have preferred title or inspection companies but shouldn't pressure you into using specific providers in exchange for better treatment. In Washington, agents must clearly identify themselves and their brokerage when advertising, and lenders must give accurate, non-misleading rate and fee information. If anyone pressures you into signing something you don't understand or discourages you from getting a second opinion, that's a strong sign to move on.

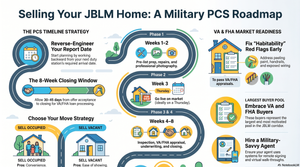

4. A Step-by-Step Process to Vet Your JBLM Real Estate and VA Loan Team

Instead of relying on random referrals or whoever answers the phone first, use a simple, structured approach to build your team.

Step 1: Start Early—Before You Get Orders If Possible

If you suspect JBLM is on your list, you can research lenders and agents two to six months before your expected PCS window, have initial conversations to outline possibilities and pre-qualification, and start watching neighborhoods and price trends online. This doesn't commit you to buying, but it gives you options when your orders drop.

Step 2: Create a Short List of 2–3 VA-Focused Lenders

Gather names from fellow service members and spouses who recently closed in Pierce and Thurston County, local military spouse Facebook groups and JBLM housing forums, and reputable local real estate agents who regularly work with VA buyers. For each lender, check reviews specifically mentioning VA loans, PCS, or "closed on time"; Washington licensing for mortgage loan originators; and how responsive they are on first contact. Then schedule brief intro calls with at least two lenders and ask the same core questions so you can compare answers fairly.

Step 3: Interview 2–3 Real Estate Agents, Not Just One

Even if your first conversation goes well, talk to a second agent. You're listening for how they explain their experience with military and VA clients, whether they ask more questions about you than they talk about themselves, and how they plan to support you if you're buying or selling remotely. A good agent will respect that you're interviewing others and won't pressure you.

Step 4: Ask Each Pro How They Work as a "Team" With the Other

Your lender and agent don't have to be from the same company, but they do need to communicate well. Ask how they typically coordinate with the other side of the transaction and whether they'll call the listing agent or lender to strengthen a multiple-offer situation. You want to hear about regular status check-ins between lender and agent, proactive communication with you about milestones, and a clear plan for remote signings or power of attorney if needed.

Step 5: Reflect on Fit, Not Just Numbers

Rates and commission structures matter, but they're not the only variable. Ask yourself whether you feel comfortable asking them basic questions, whether they explain things in a way that makes sense to you, and whether they seem to understand the military side of your life without you having to over-explain it. When you put experience, communication, VA knowledge, and PCS awareness together, you'll usually have a clear front-runner.

5. Special Considerations for Selling, Buying, and Investing Near JBLM

Many JBLM families are doing more than a simple buy or sell—you might be selling a home to buy another at your new duty station, keeping your JBLM-area home as a rental, or buying with the intention to rent it out after your next PCS. Each scenario calls for a slightly different lens when vetting your team.

If You're Selling a VA-Financed Home Near JBLM

Your listing agent should help you price based on real data—not just what your neighbor got last year—and plan for minor repairs that might surface on VA appraisals, like peeling paint, missing handrails, broken windows, or obvious trip hazards. Understand that VA doesn't automatically require everything be perfect, but the home must be safe, sound, and sanitary. Ask them how many listings they've sold where the buyer used a VA loan and how they prepare sellers for VA appraisal and possible repair requests. You also want a clear plan for coordinating showings while you're still living in the home and managing the closing if you've already PCS'd out of state.

If You're Buying With Future Rental in Mind

Tell both your lender and agent upfront if you plan to live in the property now and convert it to a rental after a future PCS, or potentially return to JBLM after retirement. Your team can help you understand VA occupancy requirements and honest timelines, choose neighborhoods and floor plans with good rental demand, and avoid properties that are difficult or expensive to maintain from afar. You'll need to comply with all loan terms, Fair Housing, and Washington landlord-tenant laws once you convert to a rental. Consulting a tax professional about rental income implications is always a good idea before making that decision. A knowledgeable agent can often connect you with local property managers before you ever need them.

FAQ: JBLM VA Loan Lenders and Agents

Should I use a lender recommended by my real estate agent or find my own?

You can do either. Many agents recommend lenders who've proven they can close VA loans on time and communicate well—a big advantage in a tight market. But you are free to shop around. A balanced approach: get quotes from the recommended lender and at least one other, compare rates, fees, and how well each understands your PCS situation, and choose based on the full picture rather than one number.

Can I buy a home at JBLM sight-unseen using a VA loan?

Yes, many JBLM buyers purchase remotely using VA financing. The keys are a VA-experienced lender who can handle e-signatures and remote closings, an agent who provides detailed video walkthroughs, inspection summaries, and honest pros and cons, and a clear understanding of your options if something serious is discovered during inspection. You should also discuss contingency plans—like a trusted local contact attending the inspection—so you're not making decisions completely blind.

Are VA loans really less competitive than conventional in the JBLM market?

They don't have to be. With the right team, VA buyers win offers every week. Your competitiveness depends more on the strength of your pre-approval, how well your agent structures and presents the offer, and the specific lender's reputation in the local market than on the loan type itself. In a community like JBLM where VA buyers are the norm, a well-prepared VA offer presented by an experienced agent is often just as attractive as a conventional one—and sometimes more so.

Bringing It All Together for Your JBLM Move

Building the right local team—a VA-savvy lender and a PCS-experienced real estate agent who communicate well and know the Thurston and Pierce County market—is the single most important step you can take before your JBLM PCS.

When you vet each professional with the questions and criteria in this guide, you'll quickly identify who has the experience, systems, and character to handle your move with care. Focus on VA track record, PCS awareness, local market depth, and ethical, transparent practice—and you'll put yourself in the strongest possible position whether you're buying, selling, or investing near JBLM.

Work With PCS Home Group's JBLM-Focused Team

At PCS Home Group, helping military families build the right JBLM real estate team is what we do every day. Our team brings:

Ashleigh Camberg's strategic leadership: Deep VA loan fluency, PCS-calibrated systems, and a commitment to matching military families with the right local professionals from day one

James Camberg's market analysis: Hyperlocal comp data and trend interpretation across Pierce and Thurston County so your decisions are grounded in real numbers

Kelly Barron's neighborhood intelligence: Micro-market expertise across the JBLM corridor so you can weigh DuPont versus Lacey versus Spanaway with clarity—not guesswork

We also maintain relationships with VA-experienced local lenders who know how to close on PCS timelines and communicate proactively. We're happy to share those connections and let you make your own choice.

Ready to start building your JBLM real estate and VA loan team?

Contact Ashleigh Camberg:

Phone: (360) 513-9034

Email: acamberg@pcshomegroup.com

Visit: pcshomegroup.com

Meet the team: pcshomegroup.com/team-page