What are the best Pierce County VA loan homes and real buyer experiences for military families relocating to JBLM in 2026?

Pierce County offers strong VA-eligible homes near JBLM with zero-down potential, competitive 2026 pricing, and solid resale demand—especially in Tacoma, Puyallup, Spanaway, Lakewood, and Dupont—when you pair the right house with PCS-smart timing and a VA-savvy team.

Why Pierce County VA Loan Homes Matter for Your 2026 PCS

If you're headed to or from Joint Base Lewis-McChord in 2026, housing is probably stressing you more than the move itself. You're trying to balance BAH, school districts, commute times, and a PCS timeline that doesn't care about interest rates or inventory. On top of that, you want to make the most of your VA loan benefit without getting stuck in a house that will be hard to sell when orders drop again.

Pierce County—and nearby Thurston County—sit at the center of JBLM life. Whether you're looking at Tacoma's historic neighborhoods, Puyallup's family suburbs, Spanaway/Lakewood's base-adjacent options, or Lacey/Olympia for a quieter feel, your decisions in 2026 will be shaped by evolving interest rates and BAH, tight but shifting inventory, VA appraisal and inspection realities, and your PCS report date, DEROS, and overlap with your current lease.

This guide breaks down the top Pierce County VA loan home areas for 2026 relocations, the types of listings that work best for military buyers, and real-world buyer scenarios that mirror what families like yours are actually experiencing—so you can make confident decisions whether you're buying, selling, or investing.

1. 2026 Market Snapshot: What VA Buyers Should Expect in Pierce & Thurston Counties

Inventory and Pricing Heading Into 2026

By 2026, Pierce County continues to be one of the most in-demand markets in Washington for VA buyers because of JBLM's steady presence.

Tacoma:

Often more affordable than King County, with higher appreciation areas near downtown and neighborhood amenities.

Puyallup / South Hill:

Popular for larger homes, newer builds, and strong school reputation.

Spanaway / Frederickson / Graham:

Often better price-per-square-foot, many newer subdivisions.

Lakewood / Dupont:

Strong demand due to proximity to JBLM gates and I-5.

Lacey / Olympia (Thurston County):

Slightly longer commute, but many military families prefer the quieter pace and planned communities.

Active but selective buyers: Even if rates fluctuate, VA buyers remain in the market. Your competition is often other PCS families with similar timelines and constraints.

Days on market varying by price point: Turn-key, well-priced homes near JBLM and major commute routes can still move quickly. Homes needing major work or with condition issues may sit longer—especially if they won't pass a VA appraisal without repairs.

What This Means for Your VA Purchase

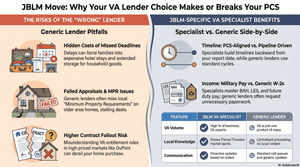

With a VA loan in Pierce County in 2026, you're typically dealing with zero-down potential (but closing costs and reserves still matter), seller attitudes toward VA that are generally positive (many local listing agents and sellers are now very familiar with VA loans), and appraisal and condition standards that require basic safety, structural soundness, and habitability as non-negotiable.

Offers with strong terms—clean contingencies, realistic closing timelines, solid pre-approval—are competitive even with zero down.

If you're also a seller in Pierce or Thurston County in 2026, you're in a market where military VA buyers are a major share of demand, especially in neighborhoods within a 30–40 minute commute to JBLM. Pricing strategically and understanding VA loan requirements upfront can widen your buyer pool.

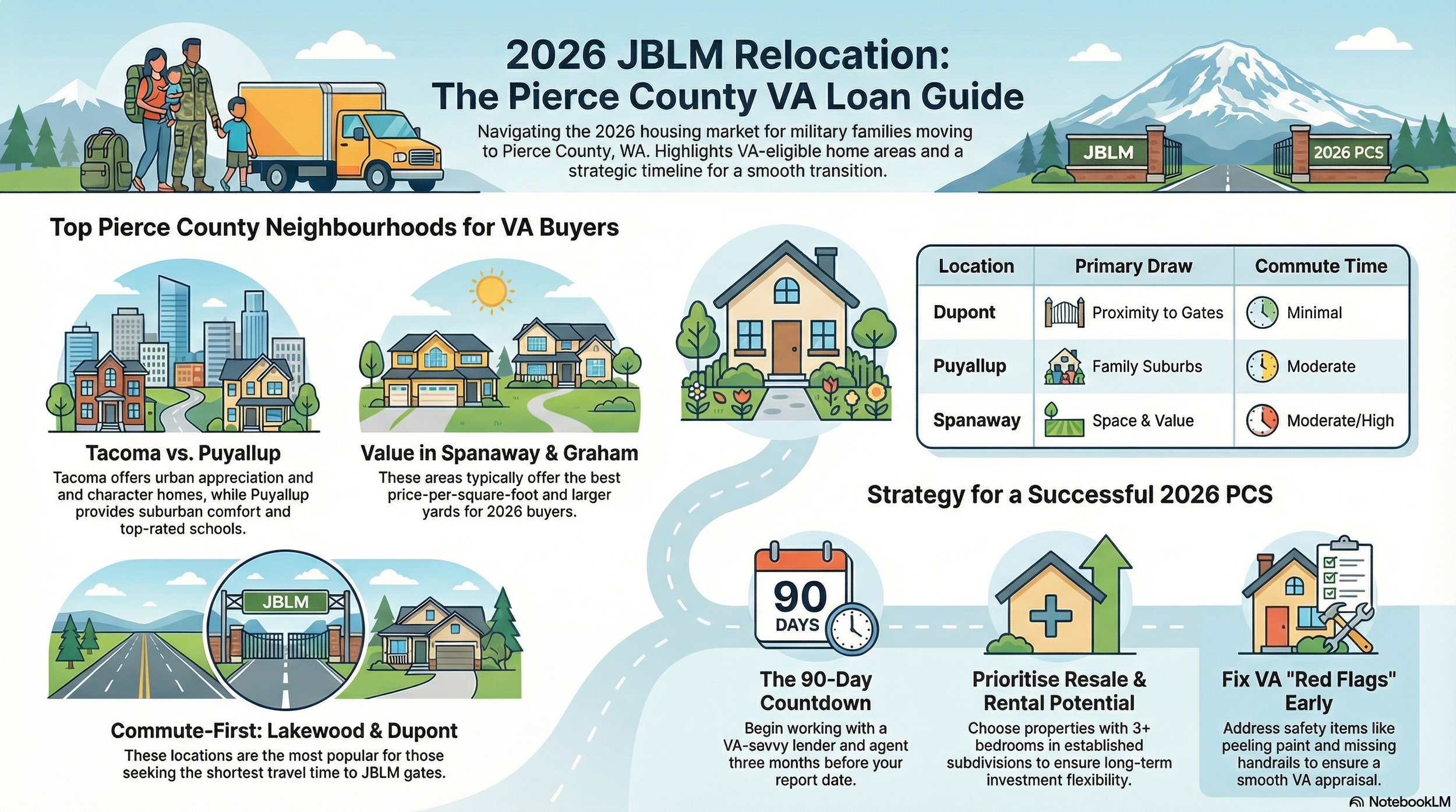

2. Best Pierce County VA Loan Areas for 2026 PCS Moves

You're not just buying a home—you're buying commute time, resale potential, and rental options if your next PCS arrives faster than expected. Here's how the main JBLM-adjacent areas stack up for VA buyers.

Tacoma: Urban Amenities and Long-Term Upside

Tacoma appeals if you want character homes, walkable neighborhoods, and better upside potential.

Pros:

Strong rental demand if you keep the home as an investment

Multiple micro-markets (North End, South Tacoma, Eastside, Hilltop, University Place nearby)

Cultural amenities, waterfront, and transit options

Typical VA-Friendly Listings:

3–4 bed, 1.5–2 bath single-family homes in established neighborhoods

Updated Craftsman homes where major systems and safety items have been addressed

Small townhomes and condos (verify HOA is VA-approved)

Watch For:

Older homes with deferred maintenance that may not clear VA appraisal without repairs

Street parking instead of garages if you need storage for gear, trailers, or multiple vehicles

Puyallup & South Hill: Suburban Feel and Schools

A favorite for many military families who want suburban comfort and good school options.

Pros:

Newer construction, cul-de-sacs, sidewalks, community parks

Larger floorplans and attached garages

Strong owner-occupant and family demographic

Typical VA-Friendly Listings:

4–5 bed, 2.5 bath homes between 1,800–2,400+ sq ft in master-planned communities

Homes built 2000s–2010s that usually meet VA minimum property requirements with minimal issues

Watch For:

HOA rules if you plan to convert to a rental later (check rental caps and parking rules)

Traffic congestion during peak commute times from South Hill to JBLM

Spanaway, Frederickson, Graham: Space and Value

If you want maximum house and yard for the money and can accept a bit more drive time.

Pros:

Often lower price per square foot

Many newer subdivisions with VA buyer history and acceptance

More room for RVs, trailers, or just breathing room

Typical VA-Friendly Listings:

3–4 bed homes, often 1,600–2,000+ sq ft, built 2000s–present

Smaller acreage or large lots where you can actually enjoy your backyard

Watch For:

Septic system condition and well water in less dense areas—VA appraisals review these closely

Road conditions and winter access if you're on more rural roads

Lakewood & Dupont: Commute-First Choices

If you want the shortest commute to JBLM.

Pros:

Some neighborhoods are minutes from JBLM gates

Popular with active-duty, reservists, and civilian DOD personnel

Rental demand stays strong close to base

Typical VA-Friendly Listings:

Townhomes and smaller single-family homes in Dupont's planned communities

Mid-century homes in Lakewood, with variable condition

Watch For:

Older homes around parts of Lakewood that may need updates to satisfy VA standards

Higher price-per-square-foot for homes closest to base

Lacey, Olympia (Thurston County): Balanced Lifestyle

If you prefer a quieter pace or are okay with a slightly longer drive.

Pros:

Planned communities, trails, and lake access in some neighborhoods

Many military families choose Lacey for schools and community feel

Solid history of VA-backed purchases; local agents and sellers are VA-savvy

Typical VA-Friendly Listings:

3–4 bed homes in HOA communities with sidewalks, parks, and good neighborhood maintenance

Newer builds that typically breeze through VA appraisal

Watch For:

Verify commute reality during the actual times you'll be driving to JBLM

HOA dues and special assessments that can affect your monthly payment

3. Real-World Buyer Scenarios & Lessons from JBLM PCS Moves

These scenarios reflect common patterns and feedback from military families buying with VA loans near JBLM—patterns you can expect to see continuing into 2026.

"We Needed Zero-Down and a Predictable Payment"

A dual-military couple PCSing from overseas wanted zero down using VA, a short commute, and the ability to rent the home out within 3–5 years.

They focused on Dupont and Lacey. What they found: Dupont provided unmatched commute times but slightly higher prices, while Lacey offered newer, slightly larger homes at similar or lower prices with a longer drive.

They ultimately chose Lacey, citing strong feeling of community, newer construction that passed VA appraisal without repairs, and good rental demand they could reasonably expect later.

Lesson for 2026: If you prioritize monthly stability and future rental potential, consider slightly further-out communities with strong neighborhood appeal—your VA loan can still stretch nicely, and you're not sacrificing long-term flexibility.

"We Needed to Sell Fast and Buy at the Same Time"

A family stationed at JBLM received orders to another state with a tight timeline. They owned a home in Puyallup and wanted to sell it and buy near their new duty station with VA financing.

What worked for them: They confirmed early that their buyer pool would heavily include VA buyers, did a pre-list walk-through specifically focused on VA appraiser hot spots (handrails, GFCI outlets, peeling paint, trip hazards, smoke/CO detectors), and addressed small items before listing, which kept the deal from stalling once a VA buyer made an offer.

Their home attracted multiple offers, including a VA buyer who could close on time. They avoided carrying two mortgages or risky short-term rentals.

Lesson for 2026 sellers: If you're in Pierce or Thurston County and your home likely appeals to military buyers, prepping for VA financing before listing can save you weeks and protect your moving timeline.

"We Wanted a House That Made Sense if We Had to PCS Early"

An Army family knew their JBLM orders could be shortened, and they were already thinking about future PCS reality. They shopped in Spanaway and Puyallup with three priorities: strong local rental demand, layout that appeals to the widest renter/buyer base (3+ bedrooms, 2+ baths), and not overpaying relative to similar nearby homes.

They focused on subdivisions where many homes were already VA-owned or previously VA-financed, and neighborhoods close to shopping, schools, and main arterials—not just "hidden gems" off a long back road.

When they did need to relocate sooner than expected, they were able to rent the home quickly to another military family and cover their mortgage plus some, thanks to choosing a neighborhood with proven rental demand.

Lesson for 2026 investors and "maybe future landlords": If there's any chance you'll keep the home as a rental, evaluate it now like a future investment, not just a personal residence. VA loans can be a powerful stepping stone to building a small rental portfolio around JBLM, but only if the property type and location support it.

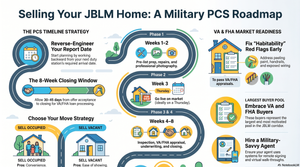

4. Structuring Your VA Loan Home Search Around a 2026 PCS Timeline

Your biggest stress point isn't just "which house"—it's when and how without derailing your orders or your family's sanity. Aligning your VA loan search with PCS realities is critical.

Step 1: Work Backwards From Your Report Date

Start with your RNLTD / report date and build a backward timeline:

60–90 days out: Begin conversations with a local VA-experienced lender and agent

45–60 days out: Actively tour homes (virtual if OCONUS) and make offers

30–45 days out: Under contract, completing inspection, appraisal, and loan underwriting

0–30 days out: Closing, receiving keys, and coordinating move-in with your HHG shipment or temporary lodging

In a competitive 2026 market, flexibility on close date can give you an edge. Many sellers also want certainty, so a VA offer with a clear timeline and strong pre-approval can beat a higher but less-secure offer.

Step 2: Know Your VA Buying Power and "Comfort Zone"

Your lender will tell you your maximum approval, but you should also define your personal comfort payment, considering BAH for your pay grade and dependency status, spouse employment and income stability, and future PCS risk and likelihood of turning the home into a rental.

Ask your lender to show you payments at multiple price points and interest rate scenarios, and estimate total cash needed at closing (even with zero down), including prepaid taxes and insurance, closing costs (and how much the seller might realistically cover), and potential rate buydown options.

Step 3: Make Your Offer VA-Strong, Not Just VA-Acceptable

A VA offer in Pierce County is normal, but you can still stand out by providing a strong pre-approval from a reputable local lender who regularly closes VA loans, offering realistic inspection timelines, and being clear and clean with contingencies—keep what protects you, but avoid unnecessary add-ons that complicate the contract.

Discuss with your agent whether to ask for seller-paid closing costs (and how that affects competitiveness), and ideal close date versus your PCS schedule and temporary housing options if closing is earlier or later than your HHG arrival.

Step 4: Plan for PCS Curveballs

PCS plans can change; your housing plan should allow for that. If you're OCONUS and delayed, consider a power of attorney (POA) for closing. If your report date moves earlier, you may need short-term lodging and a gap period; build that risk into your budget. If orders change and you can't occupy right away, talk with your lender about VA occupancy requirements and timelines—VA generally expects you to intend to occupy as your primary residence within a reasonable time, but there can be flexibility in PCS-related situations.

Being honest about your situation with your lender and agent helps them structure a plan that satisfies VA guidelines and keeps you compliant.

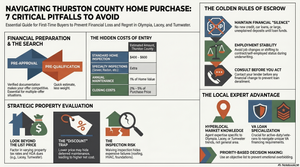

5. How Local Homeowners Can Prep Their Pierce/Thurston Homes for VA Buyers in 2026

If you're a local homeowner planning to sell in 2026, there's a good chance your buyer will be using a VA loan—especially near JBLM. Preparing with VA in mind can protect your timeline and net proceeds.

Focus on VA "Red Flag" Items First

Before you spend on cosmetic updates, address safety and habitability issues.

Add or repair:

Handrails on stairs with multiple steps

GFCI outlets near water sources (kitchen, baths, exterior)

Smoke and carbon monoxide detectors in required areas

Repair or mitigate:

Peeling or chipping paint (especially on older homes)

Tripping hazards (loose carpet, raised concrete slabs)

Missing or broken windows and locks

These are the types of issues VA appraisers are trained to notice. Fixing them up front helps avoid last-minute re-negotiations or delays.

Be Transparent About Condition and Systems

Military buyers on a tight PCS timeline are often wary of hidden issues. Providing documentation helps build trust.

Provide recent service records for roof repairs or replacement, furnace and water heater servicing, and septic pumping (if applicable). Clear disclosures of known issues, following Washington State's requirements, help buyers make informed decisions and reduce post-inspection drama.

Understand You're in a VA-Heavy Market

Pierce and Thurston Counties around JBLM are not like some parts of the country where VA is rare. Here, VA offers are common and generally well-understood by experienced local agents and lenders. A VA buyer is not inherently weaker than a conventional buyer—approval, reserves, and terms matter more than loan type.

If you're a seller who bought with VA before, you already know the benefit. You can attract more qualified buyers by being open to VA financing in your listing and working with a listing agent who understands VA guidelines and can anticipate and manage appraisal/repair conversations.

FAQ: Pierce County VA Loan Homes & JBLM Relocations

Is it harder to get a VA offer accepted in Pierce County in 2026?

In most JBLM-area neighborhoods, VA offers are normal and widely accepted. Sellers care more about your approval strength, clean and realistic terms, and your flexibility on closing and occupancy. If your offer is structured well and you're working with a VA-savvy lender and agent, you can be just as competitive as a conventional buyer.

Should I buy or rent near JBLM if I'm only expecting to stay 3 years?

It depends on your risk tolerance and long-term goals. Buying with a VA loan can make sense if you choose a home and location with proven rental demand, you're comfortable potentially becoming a landlord at your next PCS, and monthly payment (PITI + HOA, if any) lines up with both your BAH and realistic local rents.

If you want zero landlord responsibilities and maximum flexibility, renting may be the better move—but you'll miss the equity and VA-leveraged appreciation many JBLM families have seen over the past decade.

Can I use my VA loan to buy a duplex or multi-family near JBLM?

Yes, you can use a VA loan to buy a 1–4 unit property as long as you live in one of the units as your primary residence and the property meets VA minimum property requirements and lender guidelines. These can be harder to find around JBLM, and competition is strong, but for some military families they're a powerful way to combine housing and investment—especially if you plan to hold the property through multiple duty stations.

Work With PCS Home Group's Pierce & Thurston County VA Loan Experts

At PCS Home Group, we help JBLM military families navigate Pierce and Thurston County VA loan purchases and sales—every single day. Our team brings:

Ashleigh Camberg's strategic leadership: PCS timeline coordination, VA loan positioning, and buyer/seller advocacy aligned with your military life

James Camberg's market analysis: Hyperlocal comp data and trend interpretation across Tacoma, Puyallup, Spanaway, Lakewood, Dupont, Lacey, and Olympia

Kelly Barron's neighborhood intelligence: Micro-market expertise and VA-buyer success strategies throughout Pierce/Thurston

We've helped hundreds of military families buy and sell homes on time, with VA loans positioned as strengths—not obstacles—and we understand the investment potential for JBLM-area properties.

Ready to find your Pierce County VA loan home or sell before your next PCS?

Contact Ashleigh Camberg:

Phone: (360) 513-9034

Email: acamberg@pcshomegroup.com

Visit: pcshomegroup.com

Meet the team: pcshomegroup.com/team-page

Ashleigh Camberg

Military Spouse | REALTOR® | Owner, PCS Home Group

Helping VA, PCS, and First-Time Buyers Navigate Olympia and Lacey