Is it financially smarter for a military family PCS'ing from JBLM to rent out their home with a property manager or sell it outright?

A clear, numbers-based comparison of rent vs. sell—considering BAH, VA loan rules, PCS timelines, and local JBLM market trends—usually reveals which option protects your equity, cash flow, and stress level.

Why This Decision Matters So Much During a PCS

When you PCS to or from Joint Base Lewis-McChord, you don't just move households—you make a major financial decision that can affect your family for years.

If you own a home in Thurston or Pierce County—Lacey, DuPont, Lakewood, Tacoma, Puyallup, Yelm, Olympia, Spanaway, or nearby—you're probably asking:

"Should we rent it out with a property manager and keep it as an investment?"

"Or should we sell now and use the equity for our next home near the new duty station?"

"How does this affect my VA loan benefits and BAH?"

There isn't a one-size-fits-all answer. But there is a structured, local-market-based way to compare the options so you're not guessing.

Below, you'll walk through a clear framework—tailored to JBLM-area military families—to help you decide whether property management or selling your home is the better financial choice for your situation.

1. Start With the Numbers: True Cash Flow vs. True Net Proceeds

Before emotions, future plans, or "what if the market skyrockets?" questions, you need hard numbers. That means: How much would you realistically net if you sold? How much would you realistically keep each month if you rented it out?

Step 1: Estimate Realistic Rent in the JBLM Area

Don't rely on listings; look at recently rented data for your neighborhood and property type. For example, a 3-bed/2-bath in Lacey, DuPont, or Yelm near JBLM gate, with consideration for condition (updated vs. dated) and HOA rules about rentals.

You want the number you could actually secure within 30–45 days on the market, not the highest wishful-thinking rent you've seen online.

A knowledgeable local agent or property manager can usually pull a rental CMA (Comparative Market Analysis), factor in seasonality (summer PCS rush vs. mid-winter slowdown), and adjust for pet-friendly, fenced yard, AC, garage, and commute distance to McChord or Lewis.

Step 2: Calculate Your "All-In" Rental Expenses

For an accurate rent-vs-sell comparison, list every recurring expense:

Principal & interest on your mortgage

Property taxes (often escrowed)

Homeowners insurance (and landlord policy if renting)

HOA dues

Property management fee (commonly 8–12% of monthly rent in this region)

Estimated maintenance and vacancy

For maintenance and vacancy, many JBLM-area investors conservatively use maintenance/reserves at 5–10% of monthly rent and vacancy at 1 month per year (8–9% of rent) as a planning number.

Now run the math:

Monthly Cash Flow = Rent – (Mortgage + Taxes + Insurance + HOA + Management + Maintenance + Vacancy Reserve)

If this number is negative, you're subsidizing the property monthly. That might still be okay if you're building strong equity—but you must know it up front.

Step 3: Estimate Your Net Proceeds if You Sold

On the sell side, you're asking: "If we sold this home today, how much would actually end up in our bank account after closing?"

You'll want to estimate likely sale price (based on a sales CMA, not your Zillow estimate), payoff on your current mortgage(s), seller closing costs and pro-rations (title, escrow, etc.), real estate brokerage fees (consistent with Washington law and current practice), any repairs or concessions likely needed after buyer's inspection, and excise tax (Washington has real estate excise tax; amount depends on price tier and local rules).

You end with:

Estimated Net Proceeds = Sale Price – (Mortgage Payoff + Closing Costs + Fees + Excise Tax + Repair Credits)

Now you can compare Keep and rent (small monthly cash flow or small loss + long-term appreciation + principal paydown) vs. Sell (immediate lump-sum net proceeds + no ongoing responsibility or risk).

This is the baseline math you'll build on in the rest of your decision.

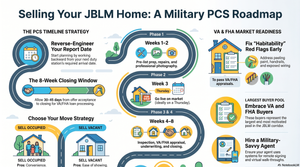

2. How Your PCS Timeline, BAH, and VA Loan Strategy Change the Equation

For a military family, this choice isn't just about today's numbers. It's about how PCS orders, BAH, and your VA loan benefits fit into a longer game plan.

PCS Timing and Risk Tolerance

Your report date and flexibility matter. If you have tight PCS dates and can't be nearby for repairs, showings, or tenant issues, you're more dependent on a property manager—and must budget accordingly. If you can stay an extra 30–60 days to prep the home for sale, stage it, and be present for contractors, selling may net you more.

Also consider: If you're PCSing OCONUS, time-zone differences and communication delays can amplify the stress of being a long-distance landlord. If you're staying CONUS but far away, ask yourself how much mental bandwidth you realistically have to manage updates and decisions.

BAH and Housing at the New Duty Station

Look at how your BAH at the gaining installation compares to local rents, local home prices, and your desire to buy again soon with your VA loan.

If renting out your JBLM-area home means you're cash-flow negative here, and you're stretching to buy at the new duty station, and you're relying heavily on BAH to cover everything, you may be over-leveraging your housing budget.

Conversely, if your JBLM-area home is cash-flow positive or neutral, and you can comfortably afford a new home (or are choosing base housing) using your BAH at the new location, then holding your JBLM home as a rental could be a smart long-term wealth play.

VA Loan: Occupancy, Entitlement, and Your Next Purchase

With VA loans, you promise to occupy the property as your primary residence. But once you've met that requirement, you can generally move due to PCS and convert the home to a rental, keeping the same VA loan in place; you don't have to refinance into a non-VA loan just because you're renting.

The key questions are: How much entitlement is tied up in this home? and Will you need your full entitlement to buy at the new station?

If your remaining entitlement is limited, your options might be to sell the JBLM home, restore full VA entitlement, and use $0 down at the new duty station, or keep the JBLM home, but then either use remaining partial VA entitlement with a down payment, or use a different loan type (FHA, conventional) for the next purchase.

Ashleigh Camberg often helps JBLM families run example scenarios with VA-experienced lenders to understand questions like: "If I keep this JBLM home, what's the maximum purchase price and down payment required for my next VA loan?" and "If I sell, how does that change my eligibility and out-of-pocket costs?"

Your VA strategy can be the tiebreaker between renting and selling.

3. Long-Term Wealth vs. Short-Term Simplicity: What Fits Your Family?

Beyond the math and VA rules, you need to think about long-term goals and current season of life.

Why Some JBLM Families Choose to Keep and Rent

Keeping your home and hiring a property manager can be appealing if you like the idea of building a small rental portfolio as you PCS around the country, you believe in the long-term growth of the JBLM/Tacoma–Olympia corridor, and you're comfortable with some level of risk and variability.

Benefits may include:

Principal paydown by tenants: Each month, some of your mortgage gets paid off with someone else's rent

Potential appreciation: Thurston and Pierce County have seen strong long-term growth, especially near JBLM and major employers

Tax advantages: In many cases, you may be able to deduct mortgage interest (on a rental property), property taxes, depreciation, and repairs and some travel related to the property (always verify with a licensed tax professional; this isn't tax advice)

But be realistic about unexpected repairs (water heaters, roofs, appliances), turnover costs (painting, flooring, deep cleaning between tenants), and occasional vacancy. If those possibilities make you extremely anxious, and you don't have reserves, a rental might not match your risk tolerance right now.

Why Others Decide Selling Is the Better Move

Selling can make more sense if you need to unlock equity to pay off debt, build an emergency fund, or fund a down payment at the next duty station, the home would be cash-flow negative as a rental and you're not comfortable subsidizing it, or you want to simplify your life and reduce moving-related stress.

Benefits of selling include:

A clean financial slate: no ongoing risk of repairs, vacancies, or tenant issues

Stronger offers on your next home with a larger down payment or fully restored VA entitlement

Emotional relief: one less thing to manage while you're adjusting to a new command, schools, and routines

For some families, especially those with young kids or a spouse deploying soon, the mental and emotional ROI of selling outweighs the potential long-term upside of holding an investment property.

Aligning the Choice With Your Specific Goals

Ask yourself: "Do we want to be long-distance landlords right now?" "Is building long-term real estate wealth a top priority at this stage, or is financial stability and simplicity more important?" "If a $5,000 roof repair popped up while we're OCONUS, would we have the cash and the calm to handle it?"

Your honest answers help you decide whether to lean toward property management or selling.

4. Understanding Property Management in the JBLM Area: Costs, Controls, and Expectations

If you're leaning toward renting your home out, you need a realistic view of how property management actually works around JBLM.

Typical Services a Property Manager Provides

A professional property manager usually handles:

Marketing and showings: Professional photos, listings on major rental sites, and coordinating tenant showings.

Tenant screening: Credit, criminal, and eviction history checks, income and employment verification, and rental history and references.

Lease and move-in: Lease preparation compliant with Washington law and fair housing rules, move-in condition report with photos, and security deposit and pet deposit handling.

Ongoing management: Collecting rent and sending owner distributions, coordinating repairs and maintenance, handling tenant questions and complaints, and enforcing lease terms and late fees.

Move-out and turnover: Move-out inspection, security deposit accounting per Washington timelines and laws, and coordinating cleaning, paint, and repairs before re-listing.

This is what allows you to PCS and still own a rental without day-to-day involvement.

What It Really Costs

Common fees in the JBLM/Thurston/Pierce County market include:

Monthly management fee: Around 8–12% of collected rent

Leasing or tenant placement fee: Often one-half to one full month's rent when a new tenant is placed

Lease renewal fee: Sometimes a smaller flat fee when renewing an existing tenant

Maintenance coordination fee: Some companies add a small surcharge on top of contractor invoices

Example: Rent of $2,300/month with a management fee at 10% equals $230/month. Annual rent of $27,600 means annual management fees of $2,760.

Over multiple years, that's significant—but you're paying for professional oversight, compliance with Washington landlord-tenant law, and your own peace of mind.

Control, Communication, and Expectations

Before hiring a property manager, clarify approval thresholds (at what dollar amount must they get your approval before authorizing repairs?), communication methods (portal, email, phone? How do they handle time-zone differences if you're OCONUS?), and emergency protocols (who decides when to send a plumber at 2 AM, and how is that billed?).

Also ask about eviction procedures (how do they handle non-payment or lease violations while protecting fair housing compliance?), inspection schedule (how often do they visually inspect the property during a tenancy?), and Fair Housing and Washington compliance (are they up to date on state landlord-tenant laws, local ordinances, and federal fair housing rules?).

A good property manager becomes your eyes, ears, and legal buffer. A poor one can erase your profits and create headaches.

5. Putting It All Together: A Side-by-Side Decision Framework

Once you understand your numbers, PCS timing, VA situation, and comfort with property management, it's time to choose.

Use this simple framework as you decide between property management vs. selling your JBLM home.

You May Lean Toward Renting With a Property Manager If:

Your estimated monthly cash flow is neutral or positive, even after management fees, reasonable maintenance reserves, and a vacancy allowance

You have 3–6 months of expenses saved as a reserve for this property

You're comfortable with long-distance landlording and trust a local professional

You don't urgently need your equity for debt payoff, next home purchase, or emergency fund

You and your spouse/partner agree that building long-term wealth through real estate is a priority and you can live with the occasional big repair or vacancy without panic

You May Lean Toward Selling If:

Your rental projection shows persistent negative cash flow, not just a small fluctuation

You don't have adequate reserves to handle major systems failing (roof, HVAC, water heater) or sudden tenant turnover

You want to restore full VA loan entitlement to buy more affordably at the next duty station

Your life circumstances (deployments, small children, medical issues, demanding tempo) mean you need to simplify, not add complexity

Your local market analysis suggests you can lock in strong equity now, and you're concerned about potential near-term softening due to interest rates, inventory, or local economic changes

Example: How Two JBLM Families Could Choose Differently

Family A:

Bought in Lacey in 2017, significant equity. Rent covers mortgage, taxes, insurance, and management with $200/month leftover. Staying CONUS with a manageable BAH vs. local cost of living at new base. Comfortable with risk, want investment properties.

Likely choice: Keep and rent with a property manager.

Family B:

Bought in DuPont in 2022 with a near-top-of-market price. Rent would be $200/month short even before reserves. Need equity for down payment in a high-cost market at the next duty station. One spouse deploying; the other juggling kids and a new job.

Likely choice: Sell now, bank the equity, reduce stress.

Both decisions are "right"—for their specific finances, PCS orders, and risk tolerance.

FAQ: Property Management vs. Selling a JBLM Home

Can I rent out my VA-financed home near JBLM after I PCS?

In most cases, yes—after you've met the move-in and primary residence requirements of your VA loan, you can PCS and convert the home to a rental. You don't automatically have to refinance out of a VA loan. However, converting to a rental can affect how much VA entitlement you have available for your next purchase, so it's smart to review your situation with a VA-knowledgeable lender before deciding.

Is it better to wait and sell after I move, or sell before I PCS?

Financially, it often depends on current local demand and seasonality, your ability to keep the home show-ready while living there, and whether you can carry two housing payments if it takes longer to sell. Many families prefer to sell before PCS if they need the equity for their next home. Others move first, then list the home vacant and staged. A local agent can run scenarios showing likely days on market and net proceeds in each case.

What if the rental doesn't cash flow but I expect big appreciation around JBLM?

Banking on appreciation alone is risky. If your monthly loss is small and you have strong savings, you may decide it's worth it for long-term upside. But if you're stretching your budget and relying on future market gains to "bail you out," that can create stress and financial strain. In that case, selling and repositioning your equity may be more prudent.

Choosing the Right Path for Your PCS, Not Someone Else's

You're not just deciding whether to rent or sell a house near JBLM—you're making a strategic choice about your family's financial future, stress level, and long-term flexibility.

When you run real numbers on cash flow vs. net proceeds, factor in BAH, VA loan entitlement, and your next housing move, and honestly assess your comfort with long-distance landlording and property management, the right option usually becomes much clearer.

If you're unsure, your best next step is to sit down with a local real estate professional who truly understands JBLM PCS timelines, VA loans, and the Thurston/Pierce County market, and a lender experienced with VA entitlement scenarios.

Ask them to help you compare "If we rent…" vs. "If we sell…" over the next 3–5 years, in simple, side-by-side numbers. From there, you can choose the path that fits your family's real goals and real life.

Work With PCS Home Group's Property Management & Sales Experts

At PCS Home Group, we help JBLM military families make informed decisions about property management vs. selling—every single day. Our team brings:

Ashleigh Camberg's strategic guidance: Side-by-side financial comparisons, VA loan strategy, and PCS timeline coordination for rent-vs-sell decisions

James Camberg's market analysis: Rental CMAs, sales CMAs, and cash flow projections based on hyperlocal Thurston/Pierce County data

Kelly Barron's investment insight: Long-term rental demand analysis and neighborhood-specific landlord considerations

We've helped hundreds of military families evaluate whether to keep their JBLM-area homes as rentals or sell before PCS—with honest, numbers-based guidance that protects both your equity and your sanity.

Ready to compare your rent vs. sell options with real numbers?

Contact Ashleigh Camberg:

Phone: (360) 513-9034

Email: acamberg@pcshomegroup.com

Visit: pcshomegroup.com

Meet the team: pcshomegroup.com/team-page

Ashleigh Camberg

Military Spouse | REALTOR® | Owner, PCS Home Group

Helping VA, PCS, and First-Time Buyers Navigate Olympia and Lacey