What are the best VA loan lenders for JBLM buyers in 2026, and how do you choose the right one for your PCS timeline and local market in Thurston and Pierce County?

A strong JBLM VA lender combines fast PCS-friendly timelines, true zero-down VA expertise, competitive rates, and local knowledge of Thurston and Pierce County—so you close on time, protect your benefits, and stay within BAH and commute needs.

Why Your VA Lender Choice Matters So Much at JBLM in 2026

If you're moving to or from Joint Base Lewis-McChord, you don't just need "a mortgage." You need a lender who understands PCS orders, tight report dates, multiple time zones, and a housing market that can shift quickly around Lacey, DuPont, Yelm, Tacoma, and Puyallup.

In 2026, interest rates, inventory, and BAH adjustments are all moving targets. Meanwhile, VA loans remain one of the most powerful tools you have as a service member or veteran: 0% down payment in most cases, no monthly mortgage insurance, flexible credit guidelines, and assumable loans that can help on resale.

But not all VA lenders are equal—especially around JBLM. Some will quote low rates but struggle to close on time. Others may not understand Washington-specific contract timelines, VA appraisal expectations in our region, or the reality of trying to buy a home while you're still stationed in another state (or overseas).

This guide walks you through the best types of VA loan lenders for JBLM buyers in 2026, the specific features you should prioritize, how local lenders compare to national brands, and how to match the right lender to your PCS situation so you don't miss your window—or overpay for your mortgage.

1. What Actually Makes a "Best" VA Lender for JBLM?

When you're stationed at or moving to JBLM, "best" doesn't just mean lowest advertised rate. It means "most likely to get you to the closing table on time, with VA benefits fully used, and your stress level under control."

Core Traits to Look For

You'll want a lender who consistently demonstrates:

True VA expertise

Not just "we do VA loans," but regularly closing VA loans in Pierce and Thurston County, comfortable with 0% down even in competitive situations, familiar with VA residual income requirements for the West region, and able to explain your COE, entitlement, and funding fee clearly.

PCS-aware timelines and systems

You need a lender who can fully pre-approve you before you arrive, offers e-signs and remote underwriting, communicates via secure portals, email, and phone within your time zone, and can coordinate with your agent when you're in the field or TDY.

Local market familiarity

Strong JBLM lenders understand typical price points near East Gate, North Fort, DuPont, Lacey, and Yelm, how VA appraisers view older homes in Tacoma vs. newer builds in Lacey, and local property taxes and HOA/road maintenance dues that affect your approval.

Why VA-Specific Skills Matter More Than Ever in 2026

In 2026, many lenders are chasing VA business because of the volume around large installations like JBLM. That creates a gap between marketing and actual competence, especially when underwriters aren't used to interpreting complex LES documents or non-taxable income, teams don't understand PCS timing, or loan officers don't know how to position a VA offer in a multiple-offer scenario.

You want a lender who can explain to a listing agent why VA is not harder than conventional when done correctly, help structure your offer to minimize out-of-pocket costs while staying competitive, and suggest realistic closing dates based on VA appraisal turn times in Pierce/Thurston.

Red Flags to Avoid

Vague answers about how many VA loans they close per year

Pushing you toward FHA or conventional "because VA is harder" without a clear, math-based reason

Over-promising closing timelines without reviewing your full documentation

Pushy sales tactics about locking rates before you're truly ready

In short, the "best" VA lender for JBLM is the one who understands both your orders and your local market as well as they understand underwriting guidelines.

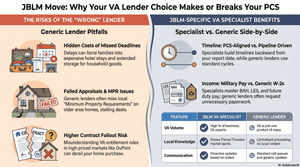

2. Types of JBLM VA Lenders: Local vs National vs Online-Only

You'll see three main categories of VA lenders around JBLM. Each can work well if you match it to your situation—but each comes with tradeoffs.

1) Local JBLM-Focused Lenders (Thurston & Pierce County)

These are banks, credit unions, and independent mortgage companies with offices in Lacey/Olympia/Tumwater, DuPont/Lakewood/Tacoma, or Puyallup/Spanaway/Graham/Yelm.

Pros:

Deep familiarity with JBLM buyers and PCS timelines

Relationships with local agents, title/escrow, and often appraisers

Easier to walk into an office if you're already in the area

Better sense of realistic closing timelines on VA loans here

Best for you if:

You want to write competitive offers quickly in a local bidding war

You're moving from base housing to buying nearby and can attend some appointments in person

You value being able to reach your loan officer directly, not a rotating call center

Potential cons:

Rates and fees can vary widely—local lenders are not automatically cheaper

Smaller operations may be slower if they're understaffed during busy PCS seasons

2) National VA-Focused Lenders

These are large lenders that heavily market VA loans nationwide and often specialize in military borrowers.

Pros:

High volume means their teams know VA guidelines well

Streamlined online portals and document uploads

Often flexible hours that work across time zones

Best for you if:

You're relocating from another base across the country and starting everything remotely

You prefer to do everything online or by phone

Your situation is relatively straightforward (stable income, solid credit, no unusual property type)

Potential cons:

Less specific understanding of Pierce/Thurston market norms

Less able to speak directly with listing agents or local parties

Appraisal, title, and closing coordination may feel more "corporate" than personal

3) Online-Only Rate Discounters and Fintech Platforms

These are digital-first lenders who advertise very low rates and fast approvals.

Pros:

Very convenient if you're tech-savvy and organized

Can be competitive on rates and some fees

Often quick with pre-approvals

Best for you if:

You're an experienced buyer comfortable driving the process

You're less worried about hand-holding and more focused on pure pricing

The property is standard (no well/septic complexities, older fixers, or VA-flaggable issues)

Potential cons:

Limited VA specialization in some cases

May struggle with nuanced issues like non-taxable BAH, second-tier entitlement, or overlapping mortgages

Listing agents in our area sometimes distrust out-of-area online lenders if communication is slow

So Which Type Should You Choose Around JBLM?

For most JBLM buyers in 2026, a strong local VA lender or a proven national VA-focused lender tends to strike the best balance of VA expertise, JBLM/PCS awareness, and solid communication with your real estate agent.

If you're doing anything more complex—such as using your VA loan again without selling your current home, buying a duplex, or navigating unique income—lean toward a lender with both VA and local specialization over a low-friction online-only option.

3. Key Features the Best JBLM VA Lenders Offer in 2026

When you compare lenders, don't just look at the interest rate. Look at what they actually provide to support your move and long-term plan.

1) Strong VA Pre-Approval (Not Just Pre-Qualification)

For a competitive offer near JBLM, you want to be fully pre-approved, meaning your income documents, LES, and BAH have been reviewed, your COE (Certificate of Eligibility) is pulled and verified, your credit has been checked and debts are accounted for, and residual income calculations for the West region are done.

A good JBLM VA lender will go a step further and run your file through VA's automated underwriting system early, flag any potential issues that might slow closing, and provide a strong pre-approval letter that gives sellers confidence.

2) PCS-Friendly Timelines and Communication

Ask lenders specific questions like "How quickly can you issue a solid pre-approval once I upload documents?" and "What is your typical closing timeline for VA loans in Pierce/Thurston?"

The better JBLM lenders will offer secure portals and e-signatures for nearly everything, provide proactive updates at each stage (underwriting, appraisal, clear to close), and coordinate with your agent on earnest money deadlines, inspection timelines, and appraisal contingencies.

3) Transparent Rates, Fees, and Credits

VA loans limit certain fees, but not all lender charges. In 2026 you should expect clear written estimates that break down interest rate options (with or without points), origination charges or "lender fees," third-party costs (appraisal, credit report, title, escrow), and any lender credits being used to offset closing costs.

The best lenders will also help you compare a slightly higher rate with more credits vs. a lower rate with higher cash due at closing, and see exactly how your BAH and other income impact your comfortable payment range.

4) Experience With Common JBLM Scenarios

You'll want a lender who can confidently navigate things like buying before you sell your current home using partial VA entitlement, using BAH and other non-taxable allowances accurately in your approval, dual-military households with staggered PCS dates or different branches, and post-ETS plans if you're transitioning to civilian work during the loan process.

Ask direct questions: "How many VA loans have you closed for JBLM buyers or sellers in the last year?" "What happens if my report date gets moved?" "Have you worked with buyers using remaining entitlement while renting out another VA-financed property?"

Confident, specific answers are what you want to hear.

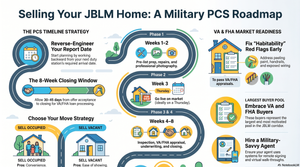

4. How to Compare JBLM VA Lenders Step-by-Step

Instead of starting with "Who has the lowest rate?" start with "Who can get me to closing smoothly and legally with my timeline?" Then compare pricing among that shortlist.

Step 1: Build a Realistic Purchase Plan

Before you talk to lenders, clarify your approximate price range (e.g., $450–550k near DuPont or Lacey), desired commute (North Gate vs East Gate vs Yelm route), whether you'll need help with closing costs, and whether you're open to assumable VA loans or focusing only on new originations.

This makes your lender conversations much more productive.

Step 2: Interview 2–3 VA-Focused Lenders

Have a consistent question list ready. Take notes on how clearly they explain things, whether they respect your comfort level and budget, and whether they answer questions directly or dance around them.

Ashleigh Camberg often helps JBLM buyers identify the right lender questions to ask based on their specific PCS timeline and property goals.

Step 3: Request and Compare Official Loan Estimates

Once you've found 2–3 lenders you trust, ask each for a Loan Estimate based on the same purchase price, estimated closing date, and VA loan structure (no points vs 1 discount point, for example).

Compare interest rate, APR (which factors in some fees), lender-specific charges, and estimated total cash to close. If one lender looks cheaper but can't explain their own numbers clearly, tread carefully.

Step 4: Weigh Service and Speed Against Marginal Rate Differences

A 0.125% difference in rate may not be worth extra stress, higher risk of delays, or weaker communication with your agent. In a PCS situation, closing on time often saves more money (and sanity) than chasing the absolute lowest possible rate.

Step 5: Confirm They Understand Washington and JBLM Requirements

Your lender should be comfortable with Washington state-specific forms and disclosures, local property tax billing cycles and impound estimates, and common HOA, condo, and manufactured home rules in Pierce/Thurston.

Strong JBLM lenders also respect Fair Housing laws (no steering based on protected classes, including military/veteran status), RESPA (transparent disclosure of all settlement costs and no illegal referral fees), and TCPA (no unwanted robocalls or texts without your consent).

Compliance isn't just legal—it's a trust signal that you're dealing with a professional, ethical lender.

5. Matching the Right Lender to Your Specific JBLM Situation

Not every military move looks the same. The best VA lender for you depends heavily on your current orders, family plans, and real estate goals.

Scenario A: PCS Into JBLM From Out of State

You're moving here with orders, maybe never having seen the base or local cities before.

You'll likely want a lender who can fully pre-approve you while you're still remote, clear max purchase price based on BAH so you don't overshoot your comfort zone, and good coordination with a local real estate agent who can preview homes or do virtual tours.

Priority features: Online document upload and e-signs, evening/weekend availability for time zone differences, and flexibility if your arrival date shifts slightly.

A strong local JBLM lender or a national VA-focused lender with proven local experience are both good fits here—just make sure your agent and lender are communicating well.

Scenario B: Already Stationed at JBLM, Moving Off Base or Upgrading

You may already know the area and commute patterns but want to buy in Lacey/Olympia/Tumwater, DuPont/Steilacoom/Lakewood, or Yelm/Roy/Spanaway/Puyallup.

You'll benefit from a lender who can help you compare renting vs buying based on projected tour length, realistic numbers for property taxes, utilities, and HOA dues in different neighborhoods, and strategies for minimal money out of pocket if you're not rolling in savings.

In this case, a local lender with a physical presence near JBLM can be especially helpful, as they often know which price ranges move fastest in each city, understand how VA appraisers view older homes vs new construction here, and have relationships with local listing agents that can reassure sellers your financing is solid.

Scenario C: Selling a VA-Financed Home and Buying Another

If you already own a VA home near JBLM and you're PCSing out, your lender needs to understand VA loan payoff and release of lien timelines, explain your options for restoring full VA entitlement, and help you troubleshoot whether it makes sense to keep the JBLM home as a rental vs sell and reuse VA elsewhere.

Key questions: "How does selling my current VA home impact my ability to use VA again?" "What if my home doesn't sell before I need to close on the next one?" "Can you help me understand second-tier entitlement if I keep this property?"

Not all lenders are comfortable with this level of entitlement strategy. That's where an experienced VA lender—ideally one familiar with JBLM—can save you stress and money.

FAQ: JBLM VA Loan Lenders and 2026 Market Questions

Are local JBLM VA lenders better than national ones?

Not automatically. A local lender who closes VA loans regularly around JBLM can offer strong advantages—better communication with local agents, realistic appraisal and closing timelines, and familiarity with Pierce/Thurston pricing. But a national VA-focused lender with deep military expertise can be equally effective if they communicate well, understand your PCS, and coordinate smoothly with your Washington real estate team. The key is VA experience plus responsiveness, not just the lender's mailing address.

How early should I talk to a VA lender before my JBLM PCS?

Ideally, start the conversation 60–120 days before you plan to buy, especially if you're relocating from another base. This gives time to pull your COE, address any credit or documentation issues, build a realistic budget based on BAH and local housing costs, and get fully pre-approved. If you're within 30–45 days of your report date, you can still buy, but your options and flexibility will be tighter, making lender speed and communication even more critical.

Can I buy with 0% down using a VA loan near JBLM in 2026 and still be competitive?

Yes, you can often be competitive with 0% down if your offer is structured well. Around JBLM, listing agents see VA loans frequently, and a strong pre-approval, realistic closing timeline, and clean contract terms can matter more than down payment size. A lender experienced in VA and the local market can help your agent present your offer so sellers understand that VA financing, when handled properly, is not riskier or slower than conventional financing.

Bringing It All Together for Your JBLM Move

Choosing the best VA loan lender for JBLM in 2026 is about far more than the headline rate. You're balancing PCS orders, family needs, commute times, BAH limits, and a dynamic Thurston and Pierce County market.

The right lender for you will understand VA guidelines and your military pay structure, respect your PCS timeline and communicate clearly with your agent, know how homes actually appraise and close around JBLM, and help you use your VA benefits strategically, not just "get a loan."

As you narrow down your options, focus on lenders who can explain things in plain language, show real experience with JBLM buyers, and provide clear written numbers you can compare. From there, you'll be positioned to close on time, protect your benefits, and find the right home for your family's next chapter.

Work With PCS Home Group's VA Loan-Savvy Team

At PCS Home Group, we work with the best VA lenders in the JBLM area—every single day. Our team brings:

Ashleigh Camberg's lender coordination: Helping JBLM buyers connect with VA-experienced lenders who match their PCS timeline, budget, and property goals

James Camberg's market analysis: Clear purchase price guidance based on BAH, local comps, and realistic closing timelines with VA financing

Kelly Barron's offer strategy: Positioning VA buyers competitively in multiple-offer situations with strong pre-approvals and smart contract terms

We've helped hundreds of military families navigate VA loan pre-approvals, lender comparisons, and PCS-driven purchase timelines—and we know which lenders actually deliver on their promises around JBLM.

Ready to connect with the right VA lender for your JBLM move?

Contact Ashleigh Camberg:

Phone: (360) 513-9034

Email: acamberg@pcshomegroup.com

Visit: pcshomegroup.com

Meet the team: pcshomegroup.com/team-page

Ashleigh Camberg

Military Spouse | REALTOR® | Owner, PCS Home Group

Helping VA, PCS, and First-Time Buyers Navigate Olympia and Lacey