Which is better for JBLM relocating families in 2026: a VA loan or a conventional mortgage, and how should you choose?

A VA loan is usually best for most active-duty and veteran buyers PCS'ing to JBLM in 2026 because of zero down, no PMI, and flexible guidelines—but a conventional loan can win if you have strong credit, larger down payment, or specific investment plans.

Why This Decision Matters So Much for JBLM Families in 2026

If you're relocating to or from Joint Base Lewis-McChord (JBLM), your mortgage choice isn't just a financial decision—it's a quality-of-life decision.

The Thurston and Pierce County markets (Lacey, Olympia, DuPont, Lakewood, Spanaway, Puyallup, Yelm) have changed a lot since 2020: home prices have climbed, interest rates fluctuate month-to-month, and competition around JBLM can be intense during PCS season.

On top of that, you're trying to time your closing with report dates, possibly buy before you sell, decide whether to keep your current home as a rental, and protect your BAH and savings for future moves or retirement.

You've probably heard, "Just use your VA loan—zero down!" from one person and, "Conventional is better if you can put money down," from another. The truth is more nuanced.

For a JBLM relocation in 2026, the right answer depends on your PCS orders timeline, your credit score and current debt, how long you plan to live in the home, whether you're building a rental portfolio or just need stability, and whether you already have a VA loan on another property.

Let's break down VA versus conventional specifically for JBLM-area buyers, sellers, and investors so you can choose confidently—without second-guessing yourself halfway through the move.

VA Loan Basics for JBLM Families in 2026

What a VA Loan Really Is (and Isn't)

A VA loan is a government-backed mortgage available to eligible service members, veterans, and some surviving spouses. It's not "free money" from the government—it's a loan from a private lender with the VA guaranteeing part of it.

For JBLM families, the VA loan is often the most powerful tool you have in this market because it's designed for mobility and affordability.

Core benefits of VA loans:

0% down payment for most price points in Thurston and Pierce County

No monthly PMI (private mortgage insurance)

Flexible credit guidelines compared to conventional

Assumable loan (a qualified buyer can take over your rate later)

Competitive rates, often better than conventional in the same market

"I work with VA buyers every single day," explains James Camberg of PCS Home Group, "and the zero-down, no-PMI combination is game-changing for military families. It means you can buy a quality home in Lacey or DuPont without draining your emergency fund—that's huge when you're facing PCS costs and unpredictable orders."

In 2026, the VA no longer has a hard loan limit for most qualified borrowers with full entitlement. That means if you qualify with income and credit, you can often buy well above previous "VA limits" without a problem. However, lenders can still set their own caps based on risk and local pricing.

What You'll Still Pay With a VA Loan

You avoid a down payment and PMI, but you don't avoid all costs. With a VA loan, you should expect:

VA funding fee (unless you're exempt): First use generally around 2.15% of the loan amount with 0% down, subsequent uses typically higher, and it can be financed into the loan instead of paid out of pocket

Closing costs: Lender fees, title, escrow, prepaid taxes/insurance, often 2–4% of the purchase price in our area

Many JBLM buyers use seller concessions or lender credits to offset closing costs, especially when cash is tight. In a softer market, it's realistic to get some or all of those covered. In a hot multiple-offer situation, you may need to plan on paying more of that yourself.

VA Loan Requirements That Affect JBLM Moves

VA loans are generous, but they have rules you need to account for in your PCS planning:

Primary residence requirement: You must intend to occupy the home as your primary residence, usually within 60 days of closing. Active-duty buyers on PCS orders to JBLM usually have no problem meeting this timeline.

Occupancy with deployments: If you deploy shortly after closing, you still qualify as long as it was your primary residence before deployment and you intend to return. A spouse can often satisfy the occupancy requirement if you're already away.

Property condition: VA appraisals look at value and minimum property standards (safety, soundness, sanitation). Homes with major deferred maintenance, missing flooring, or significant roof issues can be a problem.

In Thurston and Pierce County, that means some distressed properties, heavy fixer-uppers, or older homes in rough condition might be harder to buy with VA financing. That doesn't mean impossible—but it requires an experienced local agent and lender who know how to structure repairs and negotiations.

Conventional Mortgage Basics for JBLM Buyers and Sellers

How Conventional Loans Work in This Market

Conventional loans are mortgages that follow guidelines set by Fannie Mae and Freddie Mac. They're not government-guaranteed in the same way VA loans are, so lenders are more sensitive to risk.

In 2026, conventional loans around JBLM are typically best suited for buyers who have solid to excellent credit (usually 700+), can put at least 3–5% down (often more), don't need or qualify for VA benefits, or are focused on investment flexibility or specific price points.

Key Features of Conventional Loans

Down payment options: As low as 3% down for some first-time buyer programs, with 5–20% down being more common, especially for move-up buyers or investors.

PMI (Private Mortgage Insurance): Required when putting less than 20% down, with cost varying by credit score and down payment amount. It can sometimes be removed once you reach 20% equity (through payments or appreciation).

Property flexibility: Often more lenient on condos, townhomes, and some condition issues, and more straightforward for non-owner-occupied properties (pure rentals).

For JBLM families and local homeowners, conventional loans shine when you're buying a second home or rental that won't be your primary residence, you want to avoid the VA funding fee and can instead put more money down, or you're in a price point or situation where a seller is hesitant about VA terms and a conventional offer looks cleaner to them.

Conventional Loans and Equity Strategy

If you've owned in Lacey, Olympia, DuPont, or Puyallup for a few years, you may be sitting on significant equity. When you sell, a conventional loan on your new home can make sense if you're rolling in a large down payment and want lower monthly PMI or none at all, potentially better pricing on investment or second-home loans, or the flexibility to reserve your VA eligibility for another property later.

"When I work with clients who have built up equity from a previous tour," notes DeOnna Regan, PCS Home Group's investment strategy specialist, "we look at whether using that equity for a conventional down payment makes more sense than preserving it for emergencies or other investments. Sometimes conventional is the smarter play—it just depends on your complete financial picture."

For some JBLM officers or dual-income households with higher earnings and strong credit, a conventional loan can be a strategic tool—not just a backup plan when VA isn't available.

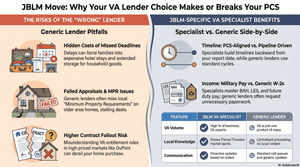

Side-by-Side: VA Loans vs Conventional for JBLM Relocations

Payment and Cost Comparison

To see how this plays out locally, imagine you're PCSing to JBLM in summer 2026 and buying a $550,000 home in Lacey or DuPont.

Scenario 1: VA Loan (First Use, Not Exempt)

Purchase price: $550,000

Down payment: $0

VA funding fee (2.15% financed): ~$11,825

Loan amount: ~$561,825

No monthly PMI

Scenario 2: Conventional Loan (5% Down)

Purchase price: $550,000

Down payment: $27,500 (5%)

Loan amount: $522,500

Monthly PMI until ~20% equity

Depending on rates and PMI pricing in 2026, here's how this often plays out:

The VA payment is usually lower, even though the loan amount is higher, because there's no PMI

The conventional payment can catch up later if you remove PMI and/or refinance, especially if rates drop

If your goal is to conserve cash and keep monthly payments predictable, VA usually wins. If you have strong savings and plan to be in the home long term, conventional can be competitive, especially if PMI falls off and you avoid the VA funding fee.

Qualification and Flexibility

Where VA loans often help JBLM families: Debt-to-income ratios (DTI) are usually more flexible than conventional, BAH can be counted toward qualifying income, and recent PCS moves and shorter job history in a new duty station can be easier to explain.

Where conventional loans sometimes outperform VA: Multiple financed properties (especially if you already have a VA loan elsewhere), second homes that aren't your primary JBLM residence, and pure investment properties you never plan to occupy.

If you're planning a long-term rental strategy—say, you want to keep your Lacey house when you PCS out and buy again at your next station—you might intentionally mix VA and conventional loans to maximize flexibility and preserve entitlement.

Appraisal and Offer Strategy in a Competitive Market

One of the most practical questions JBLM buyers ask is, "Will a VA loan hurt my chances in a multiple-offer situation?"

Here's the reality in Thurston and Pierce County: Many listing agents and sellers understand and respect VA buyers, especially in a military-heavy area. Some still assume VA is "harder" because of repairs, stricter appraisals, and perceived delays.

In a very competitive situation—especially in DuPont, North Tacoma, or hot Puyallup neighborhoods—a conventional offer can appear more flexible on as-is condition, less risky on appraisal repairs, and slightly faster in seller's eyes (even though a good VA lender can close just as quickly).

However, with the right lender and agent, VA closing timelines can match conventional, appraisal risks can be managed through buyer education and negotiation strategy, and you can strengthen a VA offer with larger earnest money, flexible closing/possession dates, and strong pre-approval.

"We help clients understand that VA loans aren't weaker—they just require more expertise," says Jordana Schneider, who works extensively with first-time VA buyers at PCS Home Group. "When your agent and lender know what they're doing, your VA offer is just as strong as any conventional offer in this market."

If your situation allows you to qualify both ways, having both a VA and conventional pre-approval in hand gives you options. You can lead with VA for cost savings on most properties, or pivot to conventional for a specific home where the seller heavily favors conventional or where condition is borderline for VA.

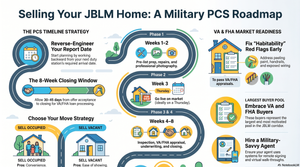

How Your PCS Timeline and Long-Term Plans Should Shape Your Choice

Matching Your Loan Type to Your PCS Orders

Timing is everything with JBLM moves. You're trying to balance report dates, school enrollments, temporary lodging, and possibly selling another home out of state.

VA loans and conventional loans can both work with PCS orders, but you need to think ahead.

If you're arriving to JBLM and want to buy quickly:

VA loan advantages: No need to wait to save a big down payment, often more forgiving if your credit took a few hits from a previous move, and BAH can be used to help you qualify.

Conventional loan advantages: If you're dual-military or dual-income with strong credit and some savings, you might use a conventional loan on a second home or future rental strategy while reserving VA for a later purchase.

If you're leaving JBLM and selling: A VA buyer assuming your existing VA loan (if applicable) could be attractive if your current rate is lower than market. A conventional offer could be slightly simpler in some cases, but in our area, VA buyers are common and usually strong.

How Long Will You Stay?

Loan choice looks different if you'll be here for 2–3 years (short tour/high chance of another PCS), 4–8 years (extended stay or possibility of retiring locally), or indefinite (settling in Thurston/Pierce County long term).

If you're likely to move again in 2–3 years, VA can be ideal because it preserves cash and keeps payments lower. You're less likely to reach 20% equity quickly, so conventional's "PMI will drop later" benefit may not kick in before you move. You can potentially convert the home to a rental later, using your VA loan to build a small portfolio over your career.

If you're planning to retire in the area and buy a "forever home," it may be worth comparing VA versus conventional more closely. You might put more cash down, reducing the gap between options. You may decide to use VA on this home and use conventional for smaller investments later—or vice versa, depending on how your portfolio evolves.

Investing and Building Wealth Around JBLM

Many JBLM families are starting to see their homes as part of a long-term wealth and retirement strategy, not just a place to live for three years.

VA loans can help you get into your first property with very little cash, let appreciation over multiple tours build your equity, and turn that home into a rental when you PCS out.

Conventional loans can help you buy additional rental properties that don't qualify for VA occupancy rules, refinance out of VA later on an existing home to restore entitlement for another purchase, and diversify your financing so you're not locked into one program.

The key for JBLM-area buyers is to think two moves ahead: Will you keep this JBLM home when you leave? Do you hope to buy at your next assignment using VA again? Are you okay delaying some investment plans to reserve VA for a later, more strategic purchase?

Align your choice now with the way you want your housing and investment picture to look ten years from now.

FAQ: VA Loans vs Conventional Near JBLM

Q: Can I have a VA loan and a conventional mortgage at the same time?

Yes. You can absolutely have a VA loan on one property and a conventional loan on another. Many JBLM families do this when they keep a prior home as a rental with a conventional mortgage, use a VA loan to buy a primary residence near JBLM, or vice versa—refinance an older VA loan into conventional to free up VA entitlement for a new purchase. The main limit is your income, credit, and total debt load, not simply the number of loans.

Q: Is a VA loan always better than a conventional loan if I qualify?

Not always. VA is usually better when you want zero down and need to protect cash, you expect to stay 3–5 years or less and won't reach 20% equity quickly, or your credit or DTI is tighter. Conventional can be better when you have excellent credit and a strong down payment, you're buying a second home or investment property, or you're in a highly competitive situation where a seller strongly prefers conventional. Running side-by-side estimates with a local lender who understands JBLM-area prices and taxes is the best way to compare.

Q: Can I use a VA loan to buy a duplex or multi-family near JBLM?

Yes—if you live in one of the units as your primary residence. VA loans can be used for single-family homes, some condos and townhomes (must meet VA approval and lender guidelines), and 2–4 unit properties where you occupy one unit. For JBLM families, this can be a powerful way to house-hack in places like Tacoma, Lakewood, or Central Lacey, where small multi-family properties exist. You benefit from 0% down (in many cases), rental income to offset your mortgage, and VA's favorable terms while starting your investment journey.

Ready to Choose the Right Loan for Your JBLM Move?

For most relocating JBLM families in 2026, a VA loan will be the best fit: it protects your cash, reduces your monthly payment, and is designed for the reality of frequent moves and PCS orders. That's especially true if you're active-duty or recently separated, you want to conserve savings for emergencies, future PCS moves, or retirement, and you're buying in typical JBLM price ranges in Thurston and Pierce Counties.

A conventional mortgage becomes more compelling when you have strong credit, steady high income, and a larger down payment, you're buying a second home or investment property that doesn't meet VA occupancy rules, or you're structuring a long-term real estate investment plan and want to preserve or re-use VA eligibility strategically.

Work With PCS Home Group's Financing Experts

At PCS Home Group, we help military families navigate the VA versus conventional decision every single day. Our team brings specialized expertise:

VA loan structuring: James Camberg has closed hundreds of VA transactions and knows exactly how to make your offer competitive

Investment strategy: DeOnna Regan helps analyze when conventional makes more sense for your long-term wealth building

First-time buyer education: Jordana Schneider and Hannah Carpenter explain the differences clearly without jargon

Portfolio planning: We help you think two moves ahead, not just this PCS

Led by Ashleigh Camberg, our team understands that loan choice isn't just about rates and fees—it's about your family's financial security and long-term goals.

Contact Ashleigh at (360) 513-9034 or acamberg@pcshomegroup.com to discuss which loan type makes the most sense for YOUR JBLM move.

Visit pcshomegroup.com to learn more about our team and services.

Ashleigh Camberg

Military Spouse | REALTOR® | Owner, PCS Home Group

Helping VA, PCS, and First-Time Buyers Navigate Olympia and Lacey